Our Vision

To provide a model of best practice and innovation in audit services in the Pacific region.Our Mission

To promote good governance, enhance transparency and accountability in the public sector.

Our Core Values

The core values uphold by our office include :- Independance

- Integrity

- Teamwork

- Respect

- Co-operative Spirit

- Looking Outwards

- Making a Difference

- Open Communications

- Professional Excellence

- Valuing Individuals

Background

- The Office of the Auditor-General is also known as a Supreme Audit Institution (or SAI) in the international auditing community. A SAI is the term given to commonly describe each country’s Government Auditor.

- The Vanuatu Office of the Auditor-General is part of the International Organisation of Supreme Audit Institutions (INTOSAI) which operates as an umbrella organization for the external government audit community.

- INTOSAI provides an institutionalized framework for SAIs to promote the development and transfer of knowledge, improve government auditing worldwide and enhance professional capacity, standing and influence of its members within their respective countries.

- The local chapter of the INTOSAI for the region is the Pacific Association for Supreme Audit Institutions (PASAI).

- International Standards for Supreme Audit Institutions (ISSAIs) are a collection of professional standards and best practice guidelines for public sector auditors, officially authorized and endorsed by INTOSAI.

- ISSAIs state the basic prerequisites for the proper functioning and professional conduct of SAIs and the fundamental principles in auditing of public entities.

- There are four levels of ISSAI standards:

- Level 1: Founding Principles

- Lima Declaration of Guidelines on Auditing Precepts

- The chief aim of the Lima Declaration is to call for independent government auditing.

- A SAI which cannot live up to this demand does not come up to standard.

- It is not enough for the SAI to achieve independence; this independence is also required to be anchored in legislation.

- Level 2: Prerequisites for the functioning of SAIs

- Mexico Declaration on the SAI independence

- INTOSAI guidelines and good practices related to SAI independence

- Values and benefits of SAIs – making a difference to the life of citizens

- Principles of transparency and accountability

- Principles of transparency – Good Practices

- Code of Ethics

- Quality Control for SAIs

- Level 3: Fundamental auditing principles

- This level sets out the fundament auditing principles for public sector auditing, financial auditing, performance auditing and compliance auditing

- Level 4: Auditing guidelines

- Detailed auditing guidelines for public sector auditing, financial auditing, performance auditing, compliance auditing and other specific subjects.

- Lima Declaration of Guidelines on Auditing Precepts

- Level 1: Founding Principles

Proposed Changes to Audit Legislation

- The current Expenditure Review and Audit Act is outdated and needs replacing. Changes are required to address the independence requirements of the Office of the Auditor-General, more specifically:

- term of the Auditor-General;

- appointment and removal of the Auditor-General;

- appointment of the technical staff of the Office and;

- the separation of the audit function from the Public Accounts Committee.

- There is currently two Bills in front of Parliament to be passed, being The National Audit Office Bill and the Public Accounts Committee Bill. These Bills have been identified by the newly elected Parliament to be passed as part of their ‘100 day plan’.

- In addition, to these Bills, changes to the Constitution is required to ratify the passing of these two Bills in order to become effective.

- The change in legislation will strengthen the role of the Auditor-General in the public sector.

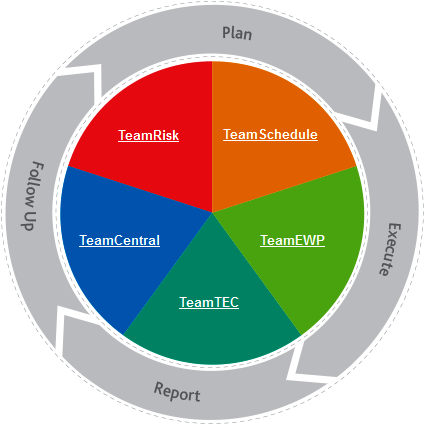

TeamMate

- It has been estimated that auditors can typically spend in excess of 40% of their time documenting and reviewing work papers and preparing audit reports. Electronic working systems often provide a single electronic audit file for each audit that can facilitate:

- Increased audit efficiency through reduced effort, time and cost;

- Improved audit effectiveness through greater compliance and alignment to ISSAIs

- More effective levels of quality assurance through detailed review of working papers

- Automatic collation and reporting of information in the audit file through the use of automatic report generation tools.

- Improved referencing and indexing, automatic linking of audit procedures to detailed write-ups and audit evidence and audit reports

- Improved audit document management and storage processes

- Security of access to audit information – only those authorised to access a specific audit file have access

- The Vanuatu Office of the Auditor-General has successfully been able to implement the use of TeamMate for all of their audits.

- TeamMate is also being utilized for its timesheet capability to enable auditors to record time spent on each audit for future planning and reporting purposes.

- In July 2016, the Office have upgraded the current version of TeamMate to 11.0 and also purchase TeamMate Analytics to further enhance the auditor’s ability to focus audit testing in high risk areas.